3 Key Takeaways

- Asset allocation is highly personal

- I keep a portfolio anchor of 50% that never changes

- The remaining 50% is adjusted every 5-10 years based on market outlook

Introduction

I have discussed using the stock market to access the power of compound interest, especially in long term retirement accounts. The most critical aspect of reaching your target return is the asset allocation of your portfolio; how you disperse your funds across different investments. The importance of proper asset allocation cannot be understated. A poor asset allocation or too much meddling can cost you a fortune. I am certainly guilty of the latter, but have become more consistent in recent years. In this article, I share what I have learned and describe my asset allocation in retirement accounts with long time horizons. My shorter term investments may differ dramatically from this strategy.

Deciding upon an asset allocation is extremely personal and dependent upon several factors such as age, risk tolerance, goals, etc. For anyone who asks, I generally recommend a simple retirement target date fund or using a robo advisor like Betterment, Wealthfront, or Schwab Intelligent Portfolios. These strategies historically return 6-8%.

I should probably follow my own advice, but as someone deeply involved with financial analytics, I have generally pursued a more custom asset allocation to try and get 9%+. I wrote this article to explain what I have learned, and also hold myself accountable to an Asset Allocation that took years to form.

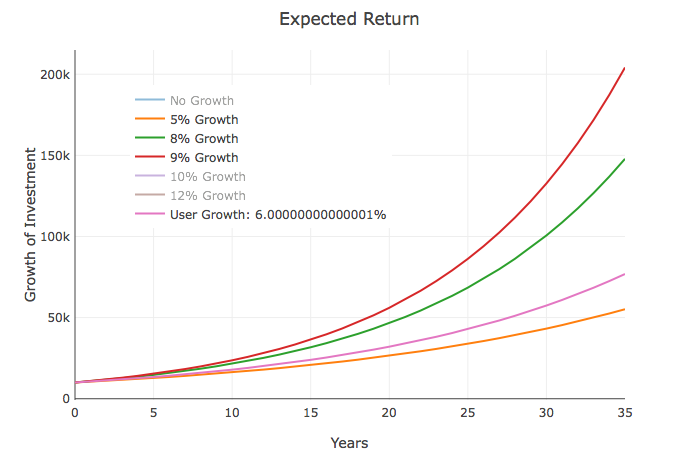

I recognize that trying to beat 6-8% returns is very challenging and could also result in 3-5% returns. That being said, due to the exponential nature of compounding, the difference between 8% and 9% is worth the risk of going from 6% to 5%. As the chart below shows, hypothetical growth of $10,000 shows a difference of $20k from 5% to 6% versus almost $60k from 8% to 9% over 35 years. For me, the risk is worth the reward.

Figure 1: Compound Interest

In my early twenties, I didn’t save enough, thinking the market was a house of cards. In my later twenties I started investing in 401ks and IRAs but was constantly meddling with my strategy. I even implemented the Value strategy discussed in The Little Book that Beats the Market, but it underperformed. I have continued to track the strategy even without being invested and the results have not been much better. Value investing has been a lagging strategy for 10 years, but maybe that indicates it will make a come back, as Value/Growth generally cycle every 5-10 years.

Regardless, I have finally arrived at an Asset Allocation that I have spent years analyzing and researching. To facilitate my research, I built a dashboard to compare portfolios and securities. The graphs below were generated from this dashboard. For my retirement accounts, I do not invest in single stocks, so I achieve my desired allocation using index funds.

First I consider my personal situation:

- Time horizon: 30-35 years

- Goal: Maximize Return and reinvest any income

- Risk Tolerance: Very Aggressive

With these considerations in mind, I have arrived at the following Asset Allocation:

- 50% in a Portfolio Anchor - US Broad Market

- 50% Tailored to a 5-10 year market outlook. As of May 2020:

- 25% International

- 15% US Sector

- 10% Gold

Portfolio Anchor - 50%

Over a 30-40 year time period, I want a position that will never change. Even in times where the entire world feels to be falling apart (e.g. 2000 dot com bust, 2008 Financial Crisis, 2020 COVID market meltdown, etc), this position is never modified. Even in the most dire circumstances, my portfolio would be 50% US Broad Market and 50% cash (or in my case gold).

For this position, I never want to think about Large Cap, Small Cap, International, Growth/Value, etc. This is designed to be the ultimate Buy and Hold position, so the selection has to be one that meets several criteria: good return profile, long track record, well diversified, consistent returns over long periods. For these reasons, I selected the US Broad Market index which holds almost every US stock, market cap weighted.

If you read my article on the US Federal Debt Bubble, you may be surprised this allocation is entirely to US Stocks, but with a 30+ year time horizon, I believe it is the safest long term bet. I will never forget one question I heard asked. “In your opinion, what are the 20 best new companies over 30 years?”, The list may change from person to person, but most of the names mentioned would be US companies (Amazon, Google, Facebook, Netflix, Uber, Beyond Meat etc). What about naming the top 20 companies in the world founded over 30 years ago? Again, the US would dominate the list (Apple, Microsoft, IBM, JP Morgan Chase, Verizon). The US market offers both growth and stability.

Not only is the US market the most stable and developed economy, but it is where new companies emerge and flourish. The US leads the world in entrepreneurship and innovation. The life blood of capitalism still runs strong in the US despite the multi-decade movement to the left. This country was built on the idea that anyone can “make it” and that culture is not changing in the near future. Regardless of the debt and potential currency concerns, there is no country that scores as highly when you want growth AND stability. Even if the US Dollar collapses, stocks in good companies will hold their value.

One can argue that most investors know this, its priced into stocks, therefore US stocks are more expensive, especially after a 10 year bull market. I tend to agree. As Warren Buffett says, “price is what you pay, value is what you get”. How much upside do the big tech names have? The IPO market doesn’t have the risk/reward it once had. The US is certainly not the best value at this point in the market cycle. It’s a very crowded trade. That is why the anchor is 50%, the remaining 50% can be tailored to align with my specific market outlook, more on that below.

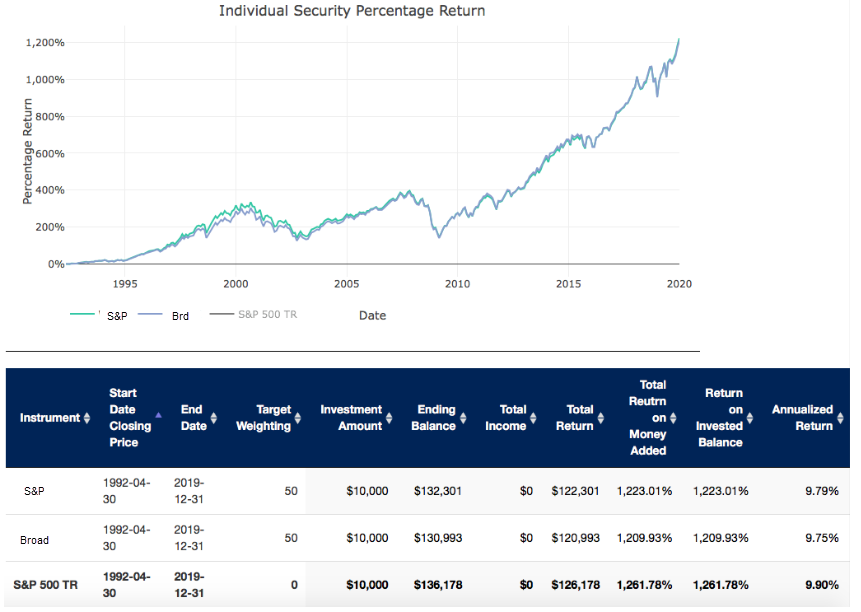

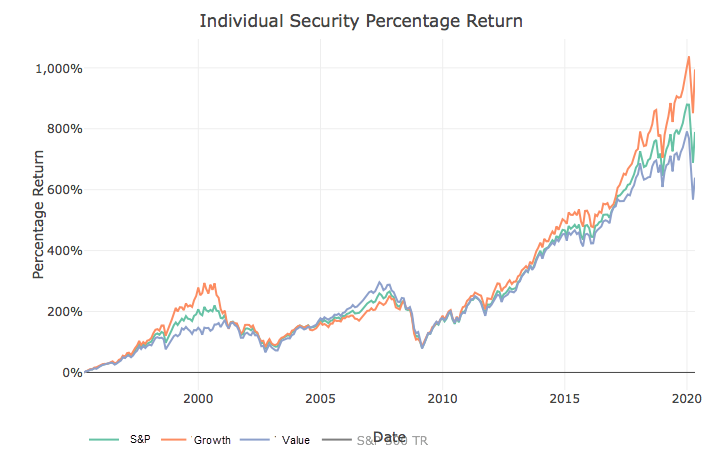

Still, the broad market has performed very well over 30 years, which included the dot com bust, the Great Recession, and now the ongoing COVID crisis (which I believe is still very early). As can be seen below, the total stock market index has just barely underperformed the S&P 500, averaging 9.75% per year compared to 9.79%.

Figure 2: The S&P 500 vs. the Total Stock Market

You may notice that the S&P has just barely outperformed the broad market, so why do I like the broad market over the S&P? For one, it’s more diversified. The S&P has only 500 companies versus 3,000 for the broad market. Albeit, the weighting is very small, but it can offer a little extra kick during different periods of the market cycle.

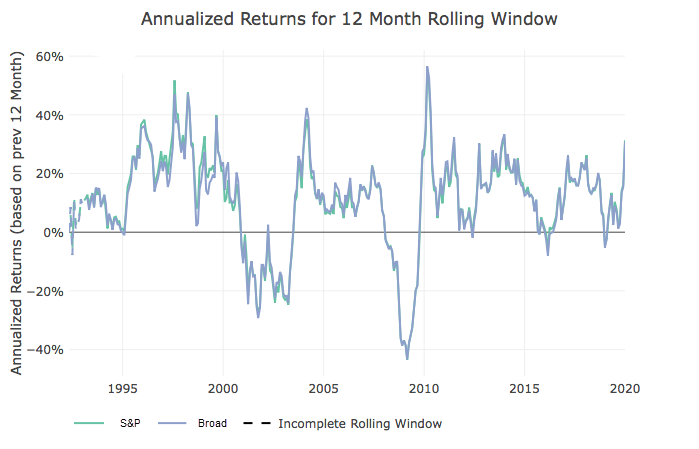

Small and mid cap generally recover faster and stronger in the early stages of a recovery. 10 years into the market recovery (pre-COVID), people were growing concerned the bull market was due for a correction and were most likely allocating more to large cap. If you go back to the end of 2014, the Broad Market index actually held a slight edge over the S&P. For me, the Broad Market offers the protection of Large Caps, with just enough exposure to small caps that it can slightly outperform. This can be seen in the rolling annualized chart below.

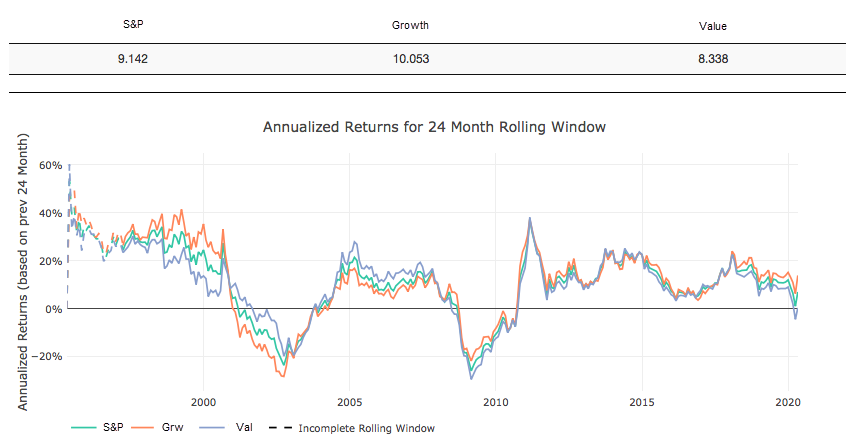

Figure 3: Annualized Rolling Returns

To recap. I am looking for a portfolio anchor that will never change for 30+ years. I want something with high reward potential, stable, long track record, and well diversified. The US Broad market hits all these requirements. Furthermore, it is super easy to buy and there are very cheap options available in both ETF and Index Mutual fund. I prefer the Mutual Funds simply because you can set up automatic dollar investing in IRAs and that is what 401ks generally have available.

Market Outlook - 50%

I would consider myself an optimist. In all human history, we have never been more prosperous as a species than right now. Despite the news headlines, this is the most peaceful time ever recorded. We are living longer, healthier lives. Even the poorest people in America have luxuries that no one could have dreamed of 100 years ago: inexpensive high quality food, modern medicine, cell phones, cars, planes, the internet, hot showers, etc. Once capitalism unleashed the human potential, we have been exponentially increasing our quality of life.

Despite government growing ever more burdensome, human ingenuity and problem solving continues improving our lives. I will save my rant on the inefficiencies of Government for a future article, but I would strongly argue we would be even more prosperous and wealthy without the massive burden.

People have predicted catastrophe for decades: food shortages, overpopulation, famine, holes in the ozone, acid rain, catastrophic global warming, etc. So far, every prediction has been incorrect. I have no doubt that we will continue to flourish. That being said, it’s not in a straight line. five steps forward (e.g. Industrial Revolution) and two steps back (two world wars). The economy and stock market is similar.

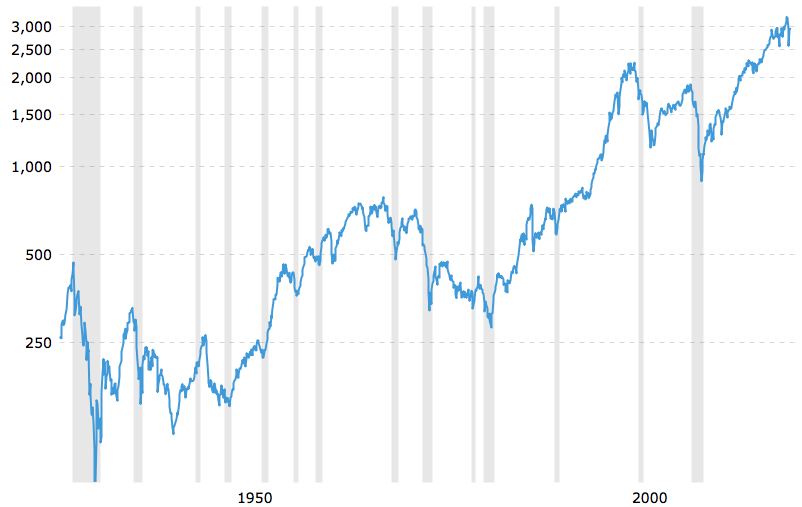

Below is a chart of the S&P 500 since 1928 using a logarithmic scale (it smoothes out the exponential aspect of compounding). While very jagged, the curve is clearly upward sloping.

Figure 4: The S&P 500 log scale

The economy and stock market rotate through different cycles overtime. These cycles can be short and seasonal (think about holiday shopping or summer travel), longer cycles such as recessions (gray lines above - every 5-10 years), and then super cycles (e.g. the Roman empire, the British empire). While I am certainly not going to argue we are nearing the collapse of the “US Empire”, each super cycle has generally ended with debt and currency devaluation.

As governments over promise and accrue more debt, they recognize that taxes will not cover obligations, so they borrow money. As debt mounts, governments print money which eventually causes a currency crisis. As I detailed in my Federal Debt Analysis and can be seen in my US Debt Dashboard, the US is well down the path of excessive debt and currency devaluation.

The recent COVID crisis has rapidly accelerated this trend, but the trend was in place long before COVID. The Federal Reserve has pushed us from bubble to bubble (dot com bubble > housing bubble > all assets bubble) using artificially low interest rates and money printing to encourage massive amounts of borrowing. Debt is essentially borrowing from the future as you consume today with future resources. Eventually the future arrives! People are worried about deflation due to COVID, but the government has too much debt and cannot handle deflation. If there is one thing governments can do better than the free market, it is inflating the money supply.

Nearly every country in the world is pursuing the same reckless policy of debt expansion and money printing. People argue that the US is the “cleanest dirty shirt in the hamper”. While this may be true for the private sector, the US Government is one of the worst offenders of debt and currency manipulation. Regardless, for 10 years investors have been pouring money into US stocks seeking the growth and stability highlighted above. I think the US market has become relatively expensive compared to many other assets. Price is what you pay, value is what you get. If you pay $100k for a really nice car that is only worth $80k, you still have a really nice car but you clearly overpaid. For this reason, my market outlook includes a smaller weighting to US stocks.

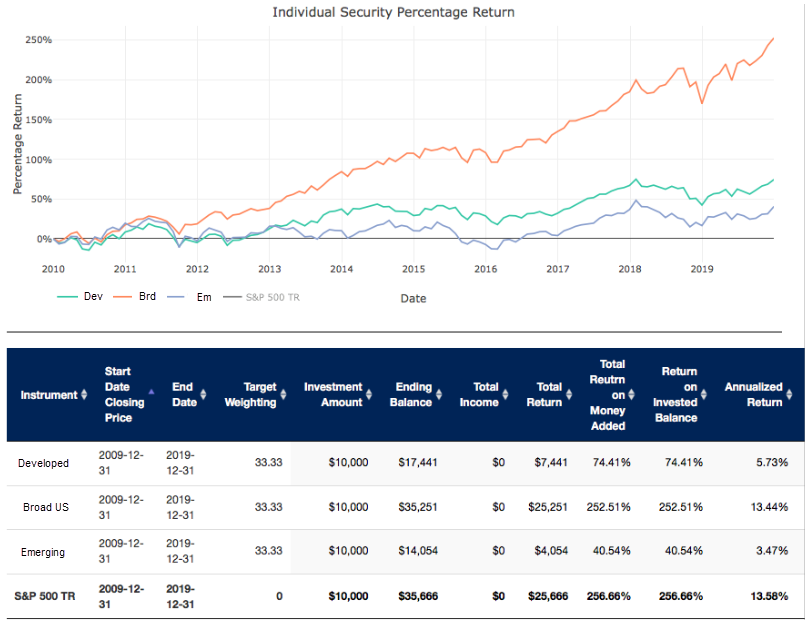

Market Outlook - International - 25%

For 10 years, International markets have dramatically underperformed US Markets. See chart below. As highlighted above, this is not without good reason. Europe is a mess and Emerging Markets are plagued by instability.

Figure 5: International vs Domestic

I think it’s possible this trend will reverse as people look for value outside of expensive US stocks. So, where can I find growth and stability outside the US? While in the US I like buying cheap index funds, I actually have mixed in actively managed mutual funds with international holdings. You pay for it (1-2% per year), but the landscape is so large that I go beyond just plain index funds.

Market Outlook - International - Growth: China - 8-9%

Reconsider the question above, name the 20 best companies since 1990. No one is naming companies from Europe (maybe Spotify?) or Japan (…?); however, you will find Chinese companies on that list (Alibaba, Tencent, Huawei, Baidu).

China has tons of issues, number 1 being run by the Communist Party. It has structural issues, concerns in the banking sector, an aging population (one child policy mistake), ghost cities, etc. That being said, people have been calling for the collapse of China for years, but it continues on. Maybe COVID with a US trade war is the straw that breaks the back, but you still have 1 billion people with a culture that prides hard work and innovation. If I want growth potential outside the US, I think China is the best bet.

China will have to adapt as companies around the world reconstruct their supply chains in response to COVID. They also have to cope with any fallout from the issues brewing with Hong Kong. This investment is not without serious risk, but it’s hard to ignore the second largest economy in the world. I think China’s best days lie ahead, even if there are some set backs along the way.

Accessing the Chinese market can be tricky, especially if you want to invest in A Shares, but options do exist.

Market Outlook - International - Stability: Developed Markets 12%

While it is hard to see the growth opportunity in International Developed markets, they definitely hold stable firms that have been undervalued for some time (Bayer, Nestle, Novartis, Toyota). I don’t see this slice of the portfolio as having the potential for high returns. Instead this is currency diversification away from the dollar.

While I hold index ETFs in some accounts, in my retirement account I have gone a bit more focused, selecting actively managed international funds.

Market Outlook - International - Risk: Emerging Markets 4-5%

Emerging markets are a tough one. Each country is so different that it’s hard to look at the sector as a single asset class. India, Brazil, Taiwan, etc all have vastly different governments and value proposition. Some emerging markets have borrowed significantly in US dollars which puts them in a dangerous position if their currencies lose value against the dollar. Regardless, every year millions more people are lifted out of poverty. This is happening in emerging markets which presents long term opportunity.

Again, I hold basic ETF index funds in some accounts, but chose actively managed for my retirement accounts. I am willing to pay the higher management fees for a strategy that closely aligns with my outlook.

Market Outlook - US Sector - Real Estate: Infrastructure 5%

Even before COVID I felt that commercial and residential real estate were vastly over priced. Now with companies around the US implementing Work From Home policies, I think the decline of high priced commercial/residential will accelerate. Regardless, I still wanted some exposure to Real Estate, especially considering I am delaying home ownership as long as possible.

With a bearish view on commercial/residential, I wanted to find other real estate investments that had good upside potential. For me the most obvious was either Marijuana or Data/Infrastructure. Marijuana seems like an obvious play as more states legalize it, pushing the Federal government to eventually follow. The data/infrastructure play is also obvious. the growth in data centers and 5G expansion are not slowing any time soon.

It’s hard to find the play in Marijuana without buying individual REITs, but a lot of REIT Funds will hold the data and infrastructure companies. Unfortunately most of these funds also hold commercial and residential REITs. For this reason I look for funds that avoid the commercial/residential REITs. The biggest concern goes back to price and value. Everyone knows about this trade, thus the price is very expensive from a Price to Earnings perspective. The good news is already priced in. Still, I think this is the safest play in Real Estate.

Market Outlook - US Sector - Large Cap/Tech 10%

This was and remains the hardest slice of my portfolio to allocate. As a highly technical data analyst, I have first hand experience with understanding, building, and implementing software. I had the privilege of working with global banks and major consulting firms. I was constantly baffled at the lack of quality technical talent. I have met very few people who can actually use Microsoft Excel proficiently, much less build software.

The value and efficiency gained by good software is incredible. You can save fortunes in salary if you have great software, yet most of the big companies I worked for were not even close to leveraging even decent software. Most of the banks I worked for still used main frames! When you look at Amazon, Google, Apple, Netflix, etc, these companies have talent and capabilities that run circles around the largest firms in other industries.

The game has changed, comparing small firms to large firms is not a linear relationship brought on by economies of scale. With the tech firms, the curve is much closer to exponential. Still, this has been priced into most of these stocks. Even with this in consideration, can Apple double in value to 2.8 trillion? I don’t think so, but it’s also hard to bet against it.

On the flip side, the performance between value and growth stocks have oscillated pretty consistently for 25 years. Looking at the chart below, you can see that Growth has really outperformed Value for the last 10 years. As stated above, there is good reason for this, but it’s hard not to think the trend will swing back towards value in the near future. Especially when you consider how expensive growth stocks have become.

That being said, the current environment still favors tech stocks. I wrestle with this constantly. Over the next 5 years, this is the position most likely to change because I have the least confidence in it.

Market Outlook - Gold: Mining companies 10%

If US Sector Large cap is the hardest decision in my portfolio, this is definitely my easiest decision. Gold is an extremely controversial investment vehicle. People don’t understand investing in a “rock that cannot be eaten”. Gold is not a stock, it does not generate revenue. Gold is a currency, in fact gold is THE currency of human history.

Based on everything written above, it’s no secret I am bearish on the US dollar. But there is not another currency on the planet that is better positioned than gold. Sure, I can use fiat currencies to buy bonds which pay a coupon (gold does not), but how much are you losing each year to inflation? Probably a lot more than the coupon.

You will notice that bonds are completely absent from this article. To be honest, for anyone under 50, I do not see the value in them. They underperform equities across most 5-10 year+ time periods, have limited upside potential, and offer incredibly low yield. With a world drowning in debt, most companies and countries are over leveraged. Just because the US won’t default on it’s debt doesn’t mean that the currency will hold value when you are paid back.

If you could find 7-8% coupon bonds with low default risk, then its a different story. But most safe bonds are offering yields barely above 1%, with a slew of government bonds offering negative yields, which means you lose money on the nominal value of your investment, much less the real value (inflation adjusted). No thank you!

Gold has replaced bonds in my portfolio. It may not generate a coupon, but it’s not a fiat currency that can be printed away. Some people may point to Bitcoin. Bitcoin and other crypto currency is a topic for another article, but the short summary is I think Blockchain is a vastly overhyped technology. Blockchain removes the need for trust and eliminates counterparty risk, but the cost is enormous. Blockchain is really just a super expensive low performance database. Not to mention, that there is nothing truly unique in the blockchain code, Bitcoin simply has first mover advantage. The tech is already older than most newer blockchains.

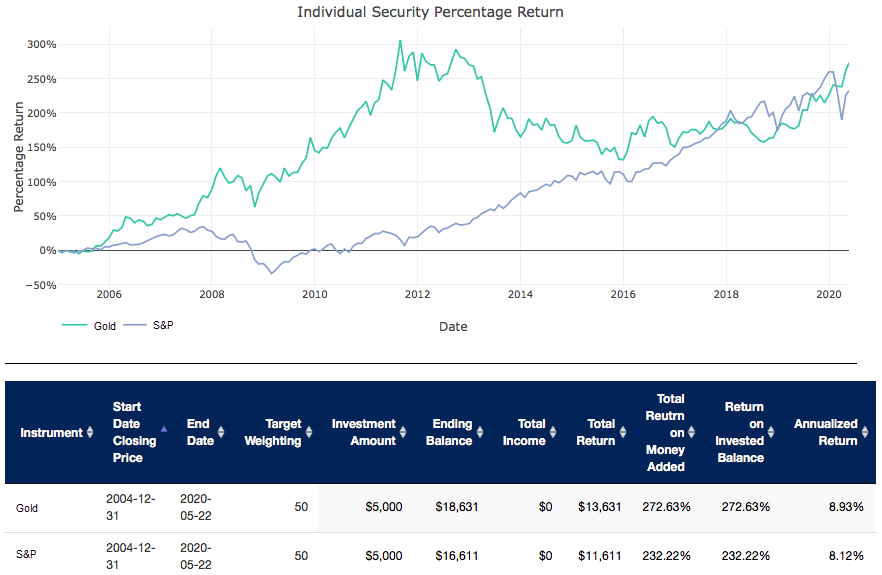

Back to gold. In a highly aggressive portfolio, I don’t think that Gold has a place in your portfolio, unless you are moving to “cash” to weather a storm (e.g. COVID volatility). A moderate portfolio (which some of mine are) deserve a gold allocation. And to be honest, it’s not a bad performing asset. Since 2005, Gold has actually outperformed the S&P 500!

For my retirement portfolio, I want to aggressively bet the price of gold continues to rise. To do this, I have selected Gold Miners. They have recently exited a brutal bear market and have even outperformed the S&P in recent years. In terms of value and upside potential, I do not see a better opportunity.

In my retirement account, I do not think this position can be taken above 10% because the sector is too volatile and the current opportunity will not last forever. In my shorter term brokerage accounts I am currently holding a much higher allocation.

Wrapping up

So this was my long winded way of saying that my target asset allocation for my retirement account is:

- 50% US Broad Market

- 10% Technology (with leverage if you have the stomach)

- 5% Data/Infrastructure REIT

- 12% International Developed

- 8% China

- 5% Emerging Markets

- 10% Gold/Gold mining stocks

This is highly specific to me, and should not be considered investment advice. But after years of research and tweaking, this is the allocation that I feel most comfortable with.

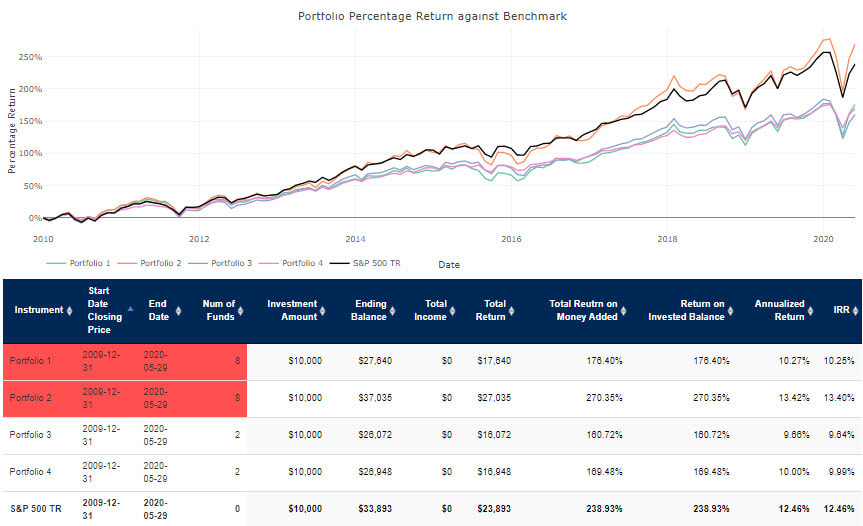

Below is the back-testing of these portfolios.

- Portfolio 1 is mostly the one above

- Portfolio 2 is the same as portfolio 1 but uses leverage for the 10% tech

- Portfolio 3 is simply 70/30 US Broad Market and All world ex-US

- Portfolio 4 is simply 70/30 S&P and Bonds

The chart starts on Jan 1, 2010 and uses annual re-balancing.

Disclosure: The content herein is my own opinion and should not be considered financial

advice or recommendations. I am not receiving compensation for any materials produced.

I have no business relationship with any companies mentioned.