Three Key Takeaways:

- The stock market has historically been a great way to access 7-10% annual returns

- Contributing on a frequent and continuous basis reduces the risk of market timing

- Investing $500 a month starting in 1975 to 2020 would have yielded $2.5M inflation adjusted

This is part 2 of a 3 part article written to demonstrate the incredible power of compound interest, the ability of the stock market to access that power, and how to determine if the stock market is better than home ownership. The ideas herein are complemented with an accompanying dashboard that can be used to enter in assumptions relevant to your situation. Technical people can find my source code on GitHub. Enjoy!

I know many people equate the stock market to gambling. The smooth returns shown in article 1 are nothing like the actual stock market. While the stock market is very erratic on a daily or even annual basis, overtime the returns become much smoother. In this article, I hope to demonstrate that even with the annual fluctuations, your money can grow incredible amounts in the stock market, especially compared to cash! The most important thing is to get invested and continue adding. When the market goes down, consider it a sale and add more. Always add, consistently overtime and history shows you will come out ahead.

What is a stock market index?

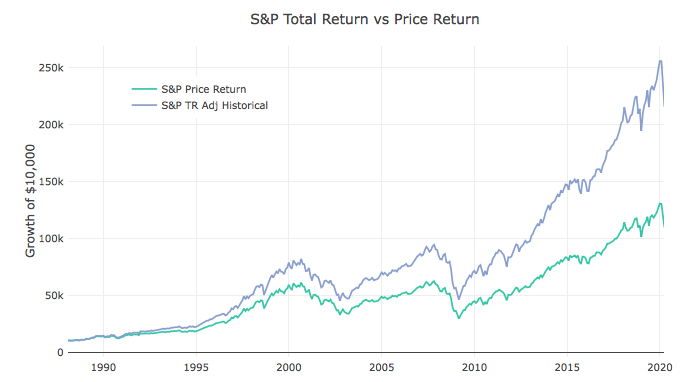

This section is a bit more financially technical so feel free to jump ahead. The S&P 500 is perhaps the most popular financial benchmark (index) in the world. The index itself goes back to December of 1927, right before the Great Depression. An important caveat is that this is a Price Return index, which means it does not consider the reinvestment of dividends. Dividends are small payments companies give to share holders to distribute excess profits. Shareholders have the option to take the dividend as cash or reinvest it back into the stock. In part 1 of this series, I discussed the massive impact of small percentage changes. Dividends have typically averaged 2% per year. The S&P Total Return Index launched in 1988 and includes dividend reinvestment. If we were to compare the difference of reinvesting dividends overtime we can compare the Price Return Index to the Total Return Index. The difference again highlights the impact of small percentage changes in total returns. Assuming a starting balance of $10,000 with no additional reinvestment, the difference between reinvesting dividends is nearly double ($250k vs $125k).

Figure 1: The impact of reinvesting dividends

This dashboard offers several indexes for hypothetical returns, but almost all of them are price return indexes. Robert Shiller has recreated an S&P total return index dating back to 1871 but has adjusted the index for inflation which pretty much negates the dividend impact in nominal terms (inflation has typically averaged 2% a year). To try and capture nominal total returns of the S&P I recreated a crude index by adding 2% to the S&P price return prior to 1988 and combined it with the actual total return index. For the purposes of this article, I will use the Shiller S&P Real total return index since it captures true gain in purchasing power, not to mention he is very distinguished Yale professor which slightly outranks my amateur financial blogger credentials.

The market could crash tomorrow!

In fact, at time of publishing in March of 2020 the stock market is crashing today. Lucky me, I get to buy assets on sale and continue converting my traditional IRA to a Roth IRA (a topic for a future article). The bottom line is that IT DOES NOT MATTER.

If you are nearing retirement and have a large portfolio that you want to protect, then I recommend talking to a professional. For anyone under 50, consider investing and adding as much as possible! If you have a large sum of cash and are scared to invest all at once, then add it slowly, maybe over 12-24 months, a very common strategy known as dollar cost averaging.

Still, it does not matter! I know I know, the market is overpriced, we are ten years into a bull market, Bernie Sanders could be the next president, the US has $23 trillion in debt with $100 trillion in unfunded liabilities, the Federal Reserve has inflated a massive asset bubble by pumping cheap money into the economy that will crash at some point, global warming, etc, etc. For any millennial it feels like a very scary time. The after shocks of the great recession are still being felt. Even so, ask your parents about the 70s and 80s (oil crisis, inflation, the Cold War, potential nuclear Armageddon) or your grandparents about the 40s, 50s, and 60s (world war 2, Korean War, Vietnam). Through all these scary times the stock market has marched higher and higher. Year after year, decade after decade.

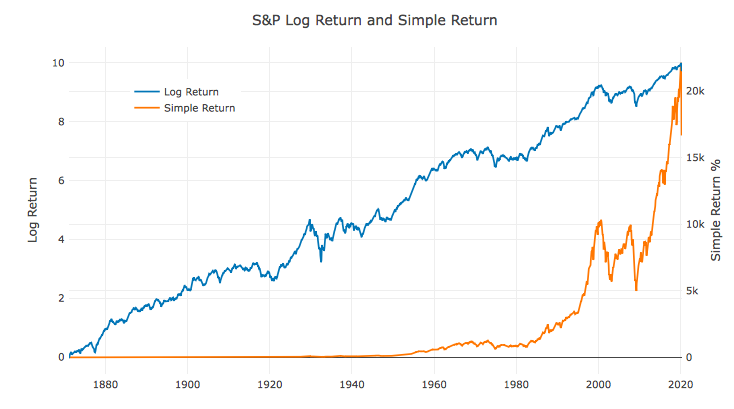

The chart below shows the long term trend of the S&P going back to 1871. Log Returns are displayed to remove the effect of compounding that essentially causes later periods to dwarf earlier periods in total cumulative return. That trend line is 140 years long. Zooming in would certainly show volatility and big down periods, but the trend has always been upward.

Figure 2: The historical return of the S&P (source Robert Shiller)

Don’t get me wrong, the US has a debt problem, which is why I am a big fan of gold. But I also have incredible faith in humanities ability to problem solve. The media sells fear, but the data tells an entirely different story.

We live in the most peaceful and prosperous time in all of human history. We are so prosperous that you have presidential candidates promising to redistribute Trillions of dollars in wealth. Agree or disagree with redistribution, just the fact the wealth exists to be distributed is evidence enough of our prosperity. Could a President get in the way with some bad policies and slow down economic growth? Absolutely. But no one is stopping the incredible growth we continue to see every year across the world. This is why, over time, the stock market has always gone up!

Even if you are like me, or one of my favorite financial commentators Peter Schiff, and believe we are on the edge of disaster, there is no better time to start investing then today. In 30 years the S&P will almost certainly be higher. Where do you think inflation shows up first? The stock market! If you still don’t believe me, we can look at the data.

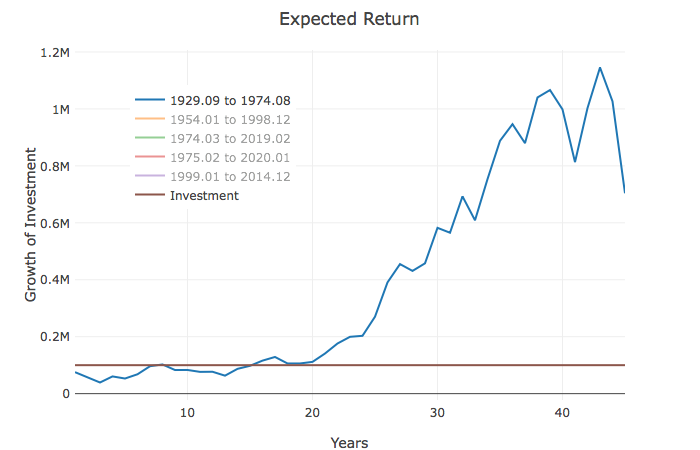

Let’s rewind the clock to 1927, the eve of the Great Depression. In hindsight, this was clearly a horrible time to start investing. Here is what 100k looks like invested all it once right before the Great Depression. 35 years later you have $888k inflation adjusted.

Figure 3: Investing 100,000 on the eve of the great depression

Sure, would it have been better to wait until 1930? Absolutely! That is obvious to see in the rear view mirror. But what if it feels like we are approaching 1927 but we are really in 2010. 2010 was a scary time, the global economy was just emerging from the Great Recession and everyone was talking double dip. Europe was a mess, the US banking sector had just been on the brink, it was hard to borrow cash, and people had lost a ton of money in real estate. I was scared, too scared to invest in the stock market.

Finally after 3 years I caved and started adding slowly to the stock market. But the whole time I was just waiting for the market to crash. I’m still waiting! Nothing about our situation is rationale. I do think we are due for a correction, and the Fed will not be able to rescue us forever. In a future article I will discuss the Fed, US debt, and asset allocation.

In this article, I am simply trying to convey the fear of the stock market that I have. Debt has been stretched to the limit, a lot of companies could fail in a downturn. But I am mid 30s and time is very much on my side so I buy… every month. Up, down, sideways, Covid 19, etc. it doesn’t matter. When it goes down, I buy a bit more aggressively, but not too much.

I built this tool exactly to help calm my own fears. I even went a step further and decided to experiment. What if this time IS different and we are set for a very rough 4 decades. What if we repeated the 15 year period of 1999-2014 three times over 45 years. For context, that means we see 3 dot com busts and 3 Great Recessions. Could it be worse than that?!? It’s possible, but certainly not probable. Well I created that scenario, and you still gain almost 5% a year! (Note this uses the S&P Total Return, not the Shiller Return). Over 45 years, your total balance will have grown from $100k to $658k. The volatility is high, but you still come out ahead.

Figure 4: 45 years of 3 dot com crashes and 3 great recessions

I know what you’re thinking, 5% is far less than the 10% we spoke about earlier. And in my previous article I specifically highlighted just how important small percentage changes make. While all that is correct if you simply max out your IRA and 401k accounts ($25,500), that 5% leaves you a balance of $3.8M on an investment of $1.1M over 45 years. A gain of $2.7M in even the most dire circumstances. This model also assumes the retirement caps stay stagnant, which they won’t!

Plus, if we have that bad a stretch over 45 years, where else are you putting money to make 5%?

- Bonds? Well a quick glance around the world shows most sovereign debt in negative territory and the US which is hemorrhaging debt at below 2% on a 30 year bond (as of March 2020).

- Cash? I’ll take 5% over 0% any day. Factor in inflation and cash goes negative.

- Gold? I love gold! To me Gold is an insurance policy against the follies of governments and central banks. But it isn’t intended to grow wealth, it preserves wealth. Gold protects you from the secret tax of inflation.

- Your house? Given the dire situation painted above, do you think a house will perform better than 5% per year! Zero chance. And to clarify, your house will only depreciate in value unless you spend money to maintain or improve it, so you are actually hoping the dirt underneath your house grows at 5% per year. Land is valuable, but I’ll bet on human ingenuity first. (More on buying a home in part 3).

I’m not trying to diminish the value of the options mentioned above as they all probably deserve some percentage of allocation (except maybe bonds if you are under 50). But we all want to enjoy our retirement. To grow your wealth, you need to capture the power of compounding, maxing out your annual rate of return. The stock market has been the best way to do that historically.

Dollar cost averaging

Let’s revisit adding money slowly overtime. Especiallly if you have a starting lump sum, this is a great way to reduce the anxiety of investing. As you slowly move into the market, if it goes up, you see growth in your account. If the market goes down, you are buying more assets with each equal purchase, so you are getting better value.

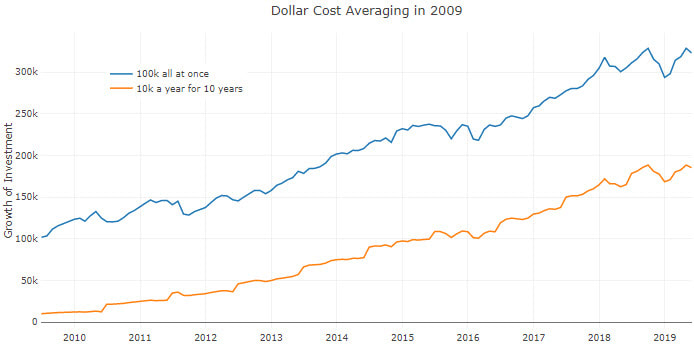

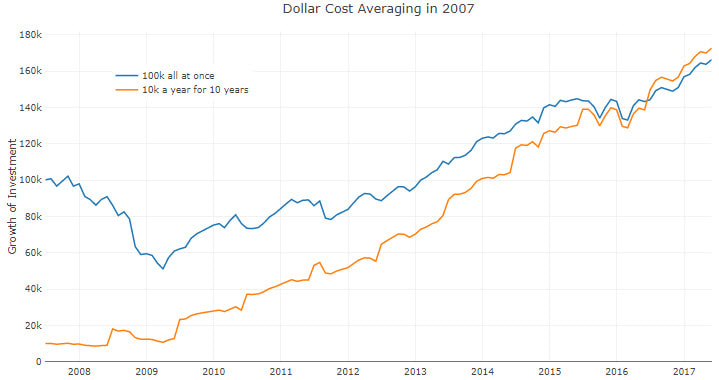

Let’s compare investing 100k all at once versus 10k each year for 10 years. In 2009 you definitely wanted to invest all at once. But what if we were in 2007? As the two charts below show, you actually have very different outcomes. Market timing is very tough, and one way to avoid the risk and nervousness around volatile markets is to use dollar cost averaging.

Figure 5: Dollar cost averaging after the Great Recession

Figure 6: Dollar Cost averaging before the great recession

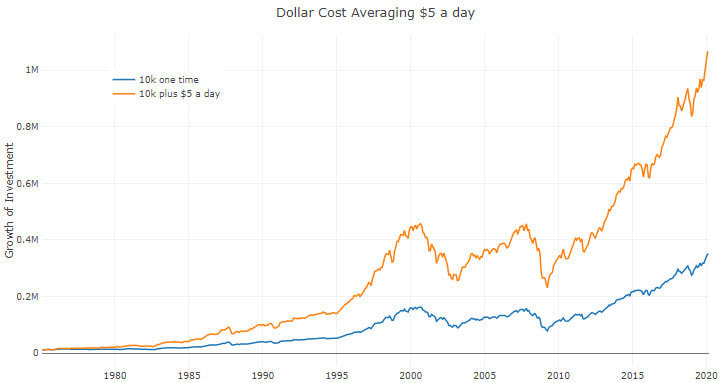

What if you have a lump sum and want to put it in the market all at once and take the risk? Okay; that’s great. But part 1 talks about small changes having huge impacts. Let’s compare two scenarios, one where you drop all 10k and let it sit for 45 years, not adding any additional funds. In the other scenario, you contribute $10k and also add $5 a day (a cup of coffee), into the stock market? Starting in 1975, the difference is incredibly stark.

Figure 7: Lump sum investing versus Lump sum and small incremental additions

10,000 sounds like a mountain next to a cup of coffee but the real mountain is in the difference between the two outcomes - 375k vs 1.1m!

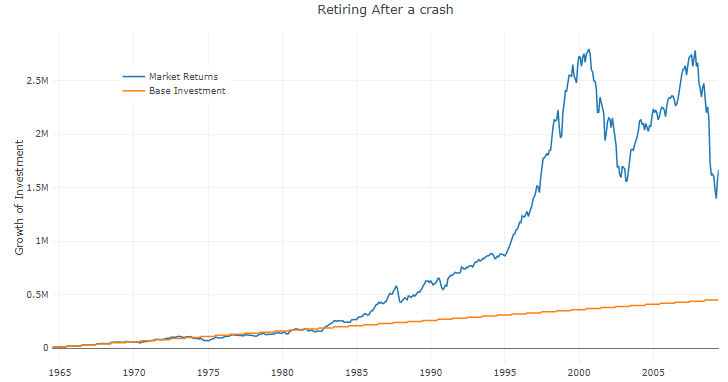

One final scenario, everything above talks about investing before a crash and how it doesn’t matter. But what if you retire right after a crash, for example someone who retires in 2009 after 45 years of diligently contributing 10,000 a year each year.

Figure 8: Retiring right after the great recession

Ouch, that definitely hurts. However, you are still left with a sizable amount to retire with (almost $1.65m). Unfortunately you actually had more at the 35 year mark in 1999. In my previous article I discussed the cost of a financial advisor. For anyone young and under $500k in assets, consider buying indexes and don’t look back. For older folks with assets to protect, an advisor can offer a lot of value and advice. Plus, after 20-30 years in the market, you have made your money so the 1% ongoing cost has less impact to your total return.

You could of course be in a standard retirement glide path fund like vanguards 2035 fund, but I personally like something a bit more tailored to me (probably at my own expense!). Make the decision that’s right for you, but blindly being in stocks for 45 years and hoping to cash out on the last day becomes a dangerous game to play. You get back to market timing.

Wrapping up

So by now, we have seen the incredible power of compound interest. I have also discussed how the stock market is the best way to gain access to compounding. Still though, many people will tell you a house is your best investment. Your house will pay for your retirement. Etc. in part 3 I will discuss why a house might not be the best investment.

Hopefully you have been convinced to start investing. The next questions is how?

For the true novice - calculate the number of years until retirement, open an IRA, buy the appropriate Vanguard Retirement Index fund and set up automatic investing.

For a slightly more custom approach - pick a Betterment, Wealthfront, Schwab Intelligent Portfolios, or any other robo advisor. Fill out the questionnaire and let them allocate capital as appropriate.

To make a few more customizations on your own - M1 Finance offers a great and easy interface to adding small dollar amounts into a custom portfolio.

What is my asset allocation? Can you or I beat the stock market (almost certainly not unless we are super lucky)? That is a discussion for a future article.

Disclosure: The content herein is my own opinion and should not be considered financial

advice or recommendations. I am not receiving compensation for any materials produced.

I have no business relationship with any companies mentioned.